America Posts

Follow American business and economic news right here on DSA Factor's Factoring 101 Blog.

Jump to a Post

- America

- Financing

- Fintech

- Insurance

December 15, 2020

Categories:

It was over a year ago that the coronavirus was first detected, and while the disease didn’t bring drastic change to America until March, that first wave is now long behind us and things have only gotten worse since the summer months. But beyond the disease which has infected millions and taken many lives, the pandemic has also been devastating to our economy. While the most visible effect of the pandemic has been bankruptcies and empty store fronts, the economic effects of the pandemic actually go much deeper than that. Prior to the bankruptcies and store closures we saw a tightening of credit insurance policies combined with an unwillingness for the industry to take on new clients. The pandemic has also led to the disappearance of supply chain financing, which had grown tremendously over the past decade, while at the same time payment terms got extended. In other words, while consumers may only see the disappearance of their favorite stores and restaurants, behind the scenes the vendors who provide stores with their merchandise have not only seen reduced business, but a lack of financing available to them.

Credit Insurance No Longer Available

Credit Insurance has long been a tool available to wholesalers. Typically, in a business-to-business transaction, the company purchasing a product will request payment terms, meaning they won’t pay for the merchandise they receive until 30 days or more after receiving it. Of course, whenever you allow someone to pay for an item after it has been received there is risk involved. For some financially strong customers that risk may be minimal, but for others that may be struggling that risk may be significant. If a company were to file for bankruptcy within those payment terms, not only would they not have to pay you, but they will probably be allowed to keep the merchandise. Should they pay you but then file for bankruptcy within 90 days, you may be required by the bankruptcy court to return those funds. This is why many wholesalers obtain credit insurance, to protect themselves in the event that one of their customers files for bankruptcy.

Credit insurance has been around for a long time, and really hasn’t changed much over the years. Credit insurance remained available and reliable throughout the recession in 2008 and even during the current “retail apocalypse” that has followed. However, due to the rapidly changing business environment that resulted from the COVID pandemic, credit insurance had to make some major changes for the first time in recent history. Near the end of March it began with the slashing of credit limits and a refusal to take on any new clients. The credit insurance companies started lowering credit limits across the board, not only on struggling businesses, if not flat out denying coverage on accounts that they had previously covered. At the same time, they also stopped taking on new clients, even abruptly ceasing communications with potential new clients that they had been working on building policies for.

It is doubtful that credit insurance companies would have lost much money had they continued business as usual. Any outstanding receivables at the time of the initial lockdowns would still need to be covered as the insurance companies can’t backdate changes in credit limits, and oftentimes even give clients a grace period before a credit limit or coverage change goes into effect. Furthermore, businesses stopped placing orders after the initial shutdown, so there really wasn’t any need to lower credit limits. As a result, credit insurance companies didn’t really protect themselves from the bankruptcies since new orders weren’t being placed and they still had to provide coverage on orders that shipped in March or earlier, assuming they were offering coverage on these companies in the first place. The end result of their policy changes was that they turned away new business, and possibly alienated existing customers.

While credit insurance is not something that is visible to consumers, it no doubt effects consumers. If wholesalers are unable to insure an account, it makes them much less likely to be willing to sell to them. This means that the retailers have difficulty stocking merchandise on their shelves and consumers have even less of a reason to shop at their stores. All of this, combined with other difficulties caused by the pandemic, makes it that much harder for a retailer to survive, and ultimately leads them down the path of bankruptcy. However, it isn’t just retailers who got hurt by the lack of credit insurance, wholesalers may have had to walk away from some of their largest customers, putting both their short-term and long-term survival in jeopardy as well.

It is important to understand however that credit insurance companies do not have direct access to a company’s payment trends or even order history when making credit decisions. Credit insurance companies rely on credit reporting in order to get their data. The credit agencies they collect their data from receive reports from actual debtors typically on a monthly basis. Therefore, not only do credit insurance companies not have real-time data to rely on, the data they receive is not their own, and in general only places outstanding receivables into 30-day aging buckets. As a result, a receivable paid one day beyond terms would appear the same as a receivable paid 30 days beyond terms, while a receivable paid 31 days beyond terms will look much worse than a receivable paid 30 days beyond terms. The only time they receive actual real-time data is when a client of theirs has to report a receivable that has become past due by a certain number of days, and later when they ultimately file a claim on a receivable that remains unpaid. The data credit insurance companies would have had access to at the start of April would have looked perfectly normal since businesses would have been closed for at most one week at that time, it wouldn’t be until new data became available at the start of May that they would have noticed a slowdown. Any claims that they would have received at the end of March or beginning of April would have been on invoices that dated back to November 2019 or earlier. So, the decisions made by credit insurance companies in late March and early April were not dictated by data, but simply by fear of the unknown.

Supply Chain Financing’s Disappearance

If tightening credit insurance policies weren’t bad enough for wholesalers, the disappearance of supply chain financing has devasted many smaller wholesalers. Larger retailers always request credit terms from their customers, typically net 30 day terms, meaning that they have 30 days to pay for their merchandise. Over the past decade, it has become increasingly popular for larger retailers to agree to pay an invoice early, oftentimes after only a week or two, in exchange for a discount. Wholesalers may be willing to give these companies a discount, somewhere around 2%, for an early payment in order to improve their cash flow, creating a win-win situation for both the wholesaler and the retailer. However, this offer of early payment is not a requirement and is solely up to the retailer as to whether or not they wish to offer it.

Supply chain financing, and Fintech in general, emerged as a result of the 2008 recession. Venture capitalists saw that financing wasn’t readily accessible to small businesses and decided to use technology to make financing safe and easy. In the years that followed 2008, our economy improved greatly and large businesses were thriving. As a result, the industry grew at a time when our economy was growing, and had never experienced an economic downturn.

Of course, prior to 2020, retailers that offered early payments would have had very little reason to stop offering it, so offers of early payment were consistently available. 2020 of course changed all that when many of these retailers were forced to suddenly and unexpectedly close their stores, as well as the corporate offices where these payments come form, for an unknown period of time. As a result, most retailers stopped offering early payments at the outset of the pandemic, putting their vendors in a difficult situation where they didn’t have access to the funds that they relied on to keep their business running. To make matters worse, with corporate offices closed and without any revenues coming in from their stores, many of the retailers simply stopped making payments, even when the invoices became due. This all happened at a time when wholesalers saw new orders completely dry up and existing orders being canceled.

To make matters worse, many wholesalers who relied on supply chain financing, never bothered to consider getting credit insurance. They didn’t see the need for credit insurance since they were getting paid early. However, just like health insurance, you still need it even if you are young and healthy because you never know what the future may have in store for you. Companies who relied on supply chain financing and didn’t bother to insure their receivables, were suddenly exposed to the fact that these companies that owe them money have now closed all their stores and that bankruptcy was a very serious possibility.

While supply chain financing was still available as a tool available to retailers, retailers no longer wished to use it. Even now, nine months after the first wave of COVID-19 swept across the nation, most major retailers have started placing orders again, but still are not offering supply chain financing to their vendors. To make matters worse, many of them have also increased their payment terms from net 30 days to net 60 days or even net 90 days, forcing their vendors to wait even longer to get paid. Prior to the pandemic, extending payment terms was sign of financial distress and imminent bankruptcy, although this year we believe that it is simply a response to the unknown as stores may have to close again should things become worse. It is possible that supply chain financing may one day be offered again by retailers, but at this point, it is very clear that it is not a reliable way for wholesalers to finance their business. Another recession, or even worse, another pandemic, could easily result in the disappearance of supply chain financing again.

An Alternative to Supply Chain Finance and Credit Insurance

The disappearance of supply chain finance as an affordable way to finance a small business has led to a huge increase in demand for accounts receivable factoring. Factoring is a lot like supply chain finance, except instead of being initiated by the retailer, it is initiated by the wholesaler. It also does not require the approval of the retailer; it is solely at the discretion of the wholesaler as to whether they wished to work with a factoring company. Therefore, wholesalers don’t need to worry as much about when the next disaster will hit, the financing that their business needs is completely within their control.

Factoring also provides access to funds 7-10 days faster than supply chain finance. Where retailers typically need to receive merchandise and check it into their system prior to making an offer of early payment to their vendors, factoring companies are willing to fund their clients the same day they ship their merchandise to their customers. That means even better cash flow than you would have received with supply chain financing.

Furthermore, if non-recourse factoring is offered, then the wholesaler also receives credit insurance on their receivables along with the improved cash flow that they receive. However, unlike credit insurance companies, factoring companies have access to real-time data that shows orders placed and payment trends, along with the data that credit insurance companies receive from credit reporting agencies. As a result, factoring companies can oftentimes approve accounts that a credit insurance company may not feel comfortable with.

Accounts receivable factoring is also available on any and all accounts that a wholesaler may sell to. Where supply chain finance is typically only available from major retailers, and credit insurance comes with minimums and deductibles that pretty much rule out smaller receivables from being insured, factoring companies are willing to work with customers of all sizes. A wholesaler who does half their business with major retailers, and the other half with small mom-and-pop shops, would have access to immediate funding and credit insurance on their entire portfolio if they choose to work with a factoring company, whereas before only half their portfolio would have had financing and insurance available.

The cost of accounts receivable factoring is very comparable to the cost of supply chain financing, and in all likelihood is much less than the cost of supply chain finance and credit insurance combined. Like supply chain financing, factoring fees are based on a percent of an invoices value, however that rate is fixed so you know exactly what to expect every time you factor an invoice and can easily build it into your pricing. With supply chain financing the percentage can change based upon the retailers needs at the time they offering early payment. If a retailer begins to struggle, or if they simply need access to working capital to fund an expansion, they can ask for larger discounts in exchange for early payment.

Credit insurance on the other hand works like any other insurance product, you pay an annual premium based on how much volume you expect to do at the beginning of the year. Larger volumes get you better rates, but you don’t get reimbursed if your sales don’t reach your expectations. Likewise, if your sales exceed your expectations you may find yourself having to purchase additional coverage at a higher rate than had you purchased more coverage in the first place. Even when there isn’t a pandemic, guessing the correct amount of coverage to get can be tricky, while the pandemic pretty much guaranteed that any companies with credit insurance way overpaid for coverage. Since factoring is based on a fixed percent of an invoices value, you only pay for what you insure, nothing more, nothing less. You also don’t need to worry about deductibles or minimums with factoring, if your factoring company approves your customer, then you are fully insured.

Is Factoring Available During a Pandemic or Recession?

Accounts Receivable Factoring is one of the oldest forms of financing and not only has survived many recessions, but has also been available throughout recessions and this current pandemic. Here at DSA Factors we have been providing factoring for over 30 years and have survived several recessions during that time period. There is no question that the COVID pandemic has been the most difficult event that we have had to deal with, but we never stopped providing financing to our clients, not even in April when things were at their worst. However, we aren’t only continuing to fund our clients, we are also accepting new clients and offering them the same great service that we provide to all of our clients. If your business has lost the financing options it had been relying on for the past few years as a result of the pandemic, please give DSA Factors a call today at 773-248-9000. We are ready and willing to provide you with the funds you need to keep your business going!

- America

- Small Business

July 15, 2020

Categories:

Economy is Slowing Down as Coronavirus Cases Climb

After the dismal months of April and May, the economy seemed to be making a recovery in June. However, as Florida quickly became the new epicenter of the coronavirus pandemic, other states have been moving to shut down sectors of their economies that they had reopened to quickly. While the data for this week is still stronger than the any of the numbers we saw in April and May, it is the weakest we have seen since the start of June. Is it just one slow week that will get corrected next week, or is it a sign that we are heading back into a recession?

Purchase Orders

Credit approval requests were way down this week as were total dollars being requested. Both figures came in at 60% of what is considered normal. Since the start of June, the lowest percentage we had seen in number of requests was 73% of normal, while for total dollars it was 78% of normal. While the number of requests being at 60% is still higher than anything we saw from the final week of March through the end of May, we did see total dollars exceed 60% of normal twice during that time period.

Purchases

Meanwhile, purchases were at 66% of what is considered normal. Also, the lowest number we’ve seen since the beginning of June. Yet this percentage was only exceeded twice between the last week of March and the end of May. While these numbers do tend to fluctuate greatly from week to week, the previous week was one of the strongest for purchase orders since the pandemic began.

Payables

If there is a silver lining this week, it would come from payables. After 5 straight weeks of growth in total outstanding dollars, total number of outstanding receivables, and total number of accounts with an outstanding balance, we saw a decline in all three of these categories last week. This week we at least saw increases in 2 of these 3 categories, total outstanding dollars and total number of outstanding receivables, with both growing by 1.6%. Total number of accounts with outstanding balances only declined by half of one percent. However, it did this as some of our oldest receivables finally got paid off.

We did see a slight uptick in current receivable, where the number of current receivables grew by 1.5% and total dollars grew by .9%. As far as what percent of total current receivables account for, the numbers pretty much remained steady from last week declining by only fractions of a percent. Current receivables still make up approximately 70% of all receivables and 81% of total dollars. Both of these percentages would be at the high end of what is considered normal.

For the second straight week we are seeing a large increase in 1-30 days late bucket. This week the number of receivables in this bucket jumped by 6.5% after a 25% increase last week. Meanwhile, total dollars in this bucket jumped by 22% after last weeks’ 60% increase. The growth in this bucket can probably mainly be attributed to growth in small business spending, as small businesses tend to pay a little bit slower than national chains. At this point receivables in the 1-30 days late bucket account for 24% of all receivables and 14% of total dollars, only slightly different from last week and still at the low end of what would be considered normal.

Once again, very little changed in the 31-60 days late bucket although both number of invoices and dollars decreased slightly. These are invoices that would have been created between mid-April and mid-May when lockdowns were in full swing. While Georgia did start their reopening on May 9th, and many other states followed them in the coming week, our data has indicated that reopening did very little to boost the economy of these states. This bucket still holds much less than half of what it normally would, which seems to indicate that if companies were unable to pay for merchandise during the lockdown, that they simply weren’t purchasing any new merchandise.

Now the very positive news comes from the extremely past due invoices. Last week we saw the number of invoices in the 61-90 days late bucket get cut in half, while total dollars declined by 40%. This week we saw the number of invoices in this bucket decline by 15% while total dollars declined by an amazing 76%. Total invoices in this bucket now account for 1.3% of all invoices and .3% of all dollars still outstanding, both of which would be considered normal. Considering that about half of these invoices would have been created before stay-at-home orders were put in place, and many of the other ones may have been for purchase orders placed prior to stay-at-home orders, this is extremely positive news.

We also saw the first significant drop in invoices that are more than 91 days past due, and this isn’t the first significant drop since the pandemic, but the first since significant drop we have seen in all of 2020. All of these invoice were not only created prior to the pandemic, but they were all already past due at the time that the first stay-at-home orders went into effect. While we only received payments on a few of these invoices, the ones that got paid were very large ones. The total number of invoices in this bucket declined by 13% this week, while total dollars declined by 22%. This is an incredibly encouraging sign that businesses that were struggling prior to the pandemic are now starting to get caught up once again.

While there is no industry that hasn’t been impacted by the COVID-19 pandemic, the industries that were hurting the most were hospitality and apparel. Of the invoices that got paid off this week that were more than 60 days beyond terms, most seemed to becoming from the hospitality industry, with the vast majority being restaurants, although also a few payments from hotels. Unfortunately, it looks like the apparel industry has been unable to recover, having already lost out on the entire spring season, and now half way through the summer with very slow sales. If schools are unable to reopen in the fall, it can have a devastating impact on the apparel industry.

Payable Trends

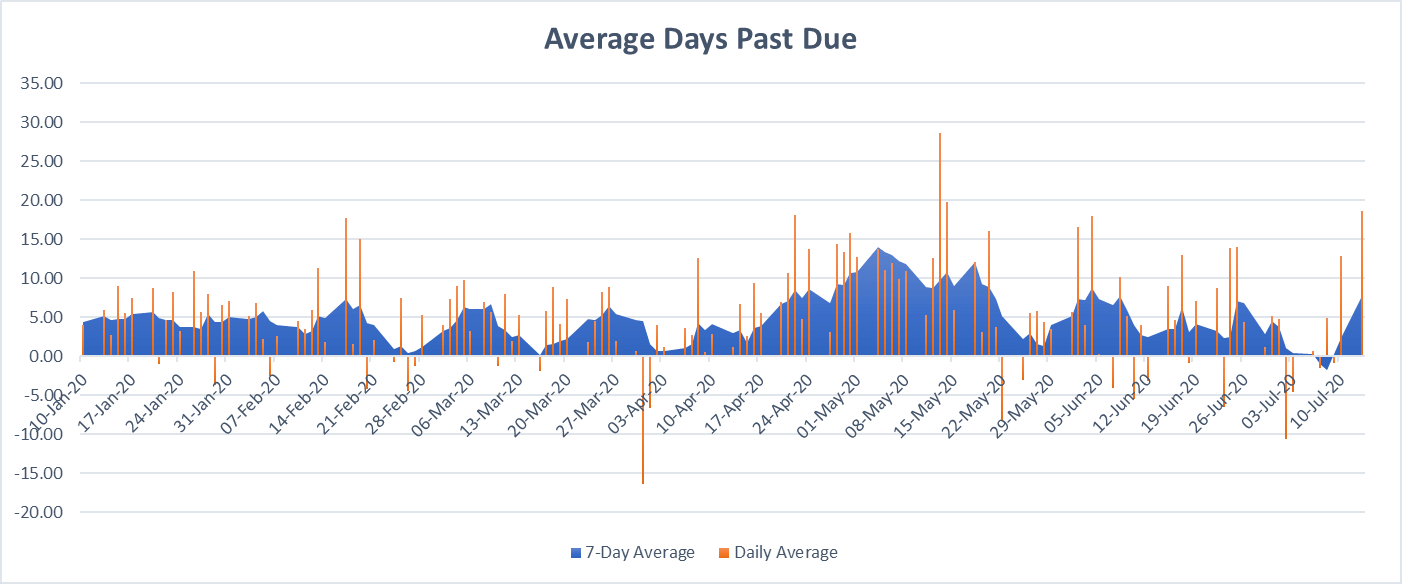

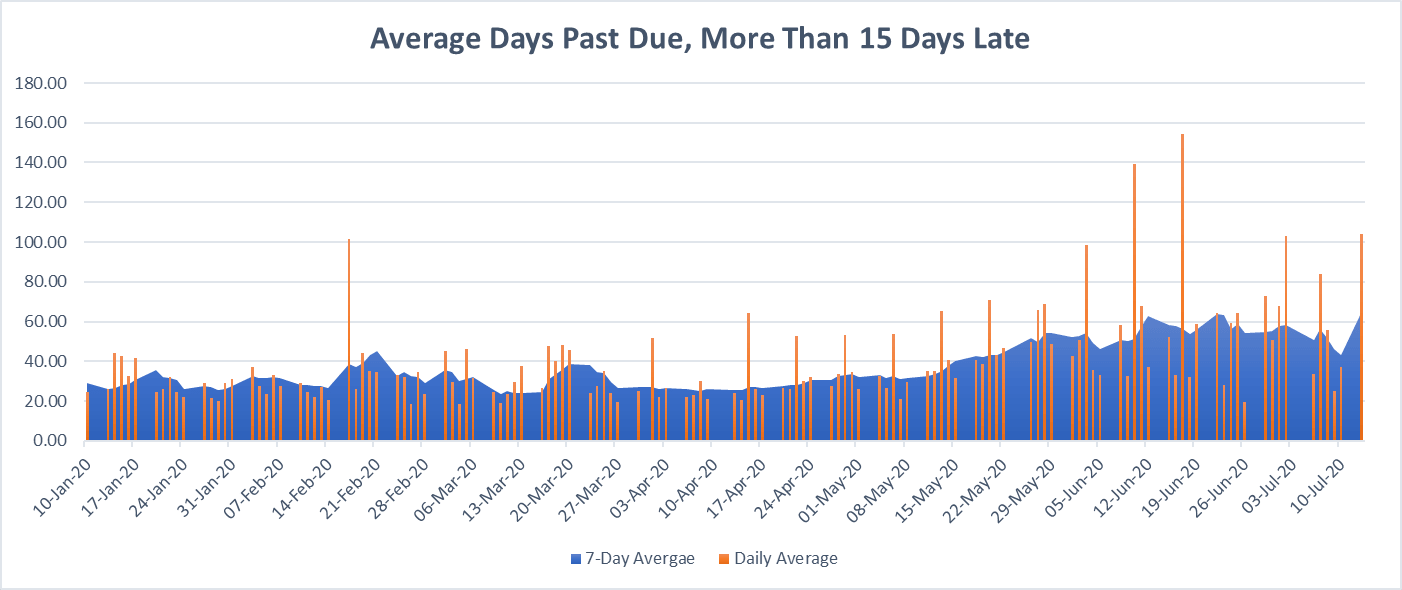

New this week, we have created two charts showing payable trends, modeled in the same way that infection charts look with 7-day rolling averages to make it easier to understand. This is very helpful given that we do not receive payments on weekends. We decided to analyze our payment data in two different ways. First, is simply by looking at all of our data, while the second only looks at companies who paid 15 days or more beyond terms. The reason for this is simple, during the pandemic, the vast majority of invoices were going to major retailers who were deemed essential businesses and typically pay their bills on time. As a result, looking at their data doesn’t really reflect the true impact that COVID-19 has had on payables. By only looking at payments that came in 15 days or more beyond terms, we are getting a more precise analysis of small businesses and the businesses that were most impacted by the lockdowns. It is important to keep in mind that we are looking strictly at the average days beyond terms for payments that we did receive, and not at how many payments we actually received. There is no doubt that we received much fewer payments while businesses were closed, so the payments that we did receive at that time would have a much greater impact on the average days beyond terms than at times when we are receiving a normal amount of payments.

As we can see from the above chart which takes all payments into consideration, it was from mid-April to the end of May that we saw the payments slow down the most, with the 7-day average peaking on May 4th at 14 days beyond terms. On average, bills got paid 4.9 days beyond terms during 2020.

However, above we are looking only at late payments, which are payments that came in 15 days or more beyond terms, we see a very different story. In this situation we see number remaining fairly level until mid-May, at which point they start to grow. Looking at 7-day averages, we actually see several peaks in this graph. The first occurred on June 12th at 63 days beyond terms, the second occurred on June 22nd at 64 days beyond terms, and then just two days ago on July 13th, at 65 days beyond terms. On average, payments that came in late in 2020, were paid 35 days beyond terms.

Obviously getting paid on one very delinquent invoice can greatly skew these numbers, as does a smaller sample size to pull from. Even though the highest numbers for late payments occurred just two days ago, at this point in time we are also receiving fewer past due payments. A perfect example of this is on June 10th when the average payment came in 5.5 days early, but the average past due payment came in 139 days late. What we can infer from these two charts is that most businesses that fell behind were able to catch up between mid-April and the end of May. At this point in time, most companies are paying bills on time, although the ones that are past due are paying bills that are extremely past due and may even pre-date the pandemic.

State-by-State

Again, very little has changed in terms of how local economies are doing on a state-by-state basis. We will continue to compare states that issued stay-at-home orders prior to March 28th to those that did so afterwards, those that started reopening prior to May 9th, the those that did so afterwards, and states that were surging as of June 23rd, to those that were remaining stable or declining. We will also look at the economies of Arizona, Florida, Louisiana, South Carolina, and Texas, five of the states that are experiencing some of the largest outbreaks at this time.

In states that implements stay-at-home orders prior to March 28th, between March 28th and May 9th, businesses in these states operated at 74% of normal levels. Since May 9th they have been operating at 96% of normal levels, same as last week. Meanwhile, businesses in states that didn’t implement orders until after March 28th, only operated at 22% of normal levels prior to May 9th, and 68% of normal levels after May 9th, which is up 1% over last week.

In states that started the reopening process prior to May 9th, businesses in these states were operating at only 25% of normal levels prior to May 9th. They are now operating at 53% of normal levels since May 9th, a 3% increase over last week. However, businesses in states that waited until after May 9th to start their reopening process were operating at 61% of normal levels before May 9th, and have been operating at 99% since May 9th, a 1% decrease since last week.

In states that were surging as of June 23rd, businesses had been operating at 49% of normal levels prior to May 9th, and since have been operating at 65% of normal levels, a 1% increase over last week. In states that had COVID-19 under control as of June 23rd, businesses were only operating at 44% of normal levels prior to May 9th, since that time they have been operating at 113% of normal levels, same as last week. It is important to note that many of the states that had stable or declining infection rates as of June 23rd, now have rising infection rates.

In Arizona, Florida, Louisiana, South Carolina, and Texas, businesses were operating at a dismal 18% of normal levels prior to May 9th, and since have recovered to 54% of normal levels. That is a 6% increase over last week’s data, but it will be interesting to see if they can maintain that pace as the infection rate in these states is rivaling the infection rate in New York at the start of the outbreak, and Florida just recently set the record for the largest number of infections in a single day for any state.

It is still very clear that a state’s ability to contain an outbreak is directly related to how strong its local economy is. It is also clear that by correcting missteps in containing the virus can also help to correct the economy, as can be seen in our comparison of states that were surging as of June 23rd to those that weren’t. Despite this week’s slight downturn, it does appear that businesses have found their new normal. However, this week we have seen several large school districts, including Los Angeles, announce that they will not be returning to in-person learning next month. Will the economy be able to keep up this pace if parents are unable to return to work, or is the downturn from this week a sign of what is going to happen a month from now if millions of children are unable to return to school.

- America

- Small Business

July 8, 2020

Categories:

The Economy is Stabilizing as the Pandemic Intensifies

There are now over three million Americans who have been infected with COVDI-19, yet as the pandemic rages on, the economy seems to have stabilized. Once again very little has changed this past week for the economy according to our data. While the economy has yet to make a full recovery, it does seem that retailers in states that have done a good job controlling the coronavirus may have returned to normal levels of business. However, as infection rates continue to skyrocket across most of the South and West, the retailers in these states are still suffering.

Purchase Orders

Credit approval requests were up again this week with the number of requests at 81% of normal levels, we’ve only seen the number of approvals reach this level once before and that was during the first week of June. Meanwhile, dollars requested reached 93% of normal levels, which isn’t a peak, but still very high.

Purchases

Purchases jumped significantly last week reaching 92% of normal levels, the highest level yet since the pandemic began if we don’t include extremely large orders that have skewed the numbers. This is a very promising number and falls in line with some of the approvals numbers we’ve seen over the last few weeks.

Payables

Payables continue to look good. After 5 straight weeks of continual growth in total outstanding dollars, we experienced a 4.5% decline this week, despite some of our highest purchase levels yet. While this would imply that more invoices got paid off than were purchased, interestingly the total volume of current receivables declined by 6% while the total number of past due receivables increased by 2.5%. This would mean that we must have received a large number of payments prior to the invoices becoming due this week. We are saw a 4% decline in both the number of open receivables and number of accounts with open receivables, marking the first time we’ve seen these numbers decline in quite a few weeks now.

Despite the decline in current receivables, current receivables still make up 70% of all receivables and 82% of total dollars. Both of these numbers would be at the high end of what is considered to be normal. So, it still appears to be the case that companies that are placing orders have the ability to pay for them in a timely fashion. Furthermore, current dollars are still at 92% of where they were on March 1st, our last data point before the pandemic took a major toll on the economy.

Ever since reaching their peak in mid-April, the 1-30 days late bucket had been in decline until last week when the number of invoices grew by 25% and dollars grew by 60%. This week continued that growth in this bucket but at a slower rate. The number of invoices that are 1-30 days beyond terms grew by 10%, while total dollars grew by 12%. Despite two straight weeks of growth, invoices in the 1-30 days late bucket still only account for 23% of all invoices and 12% of all dollars. Both of these percentages would be at the low end of what is considered normal. Again, the growth in this bucket can most likely be attributed to the growth in the current bucket that began in mid-May and continued throughout June. For that reason, it would be safe to assume that we will be seeing continued growth in this bucket throughout July.

The 31-60 days beyond terms bucket remained stable this week, with virtually no change in terms of number of number of invoices or dollars. Al of these invoice would have been created between early April and early May, at the height of the pandemic, so companies placing orders at that time would have been well aware of the difficulties that they would be facing. As a result, this bucket still holds much less than half of what we would consider to be normal, so not seeing any change isn’t really a cause for concern.

The positive news this week occurred with invoices that are severely past due. Invoices in the 61-90 days late bucket were cut in half, and total dollars in this bucket declined by 40%. These invoices now make up 1.5% of all invoices and 1.3% of all dollars, percentages that would both be at the high end of what is considered normal. These invoices would have mostly been created prior to stay-at-home orders being enacted, and all of them would have become due after non-essential businesses would have been forced to shut their doors. To see these numbers as drop significantly as they have is a major sign that businesses have been able to recover.

Unfortunately, we saw virtually no change in invoices that are 91 days or more beyond terms. In fact, we’ve seen virtually no change in this category going all the way back to February 1st. These are all accounts that were already past due (some severely past due) at the time that stay-at-home orders were issued and businesses were forced to close their doors. It is not surprising that businesses that were already struggling prior to the pandemic would continue to struggle at this time.

State-by-State

Nothing much has changed in terms of which states’ economies are doing better. It still appears to be the case that the states that took greater precautions and had greater success in slowing the spread of the coronavirus, also managed to minimize the blow on their local economy. We will continue using the 3 dates that we have been looking at in order to make comparisons. We will be comparing states that issued stay-at-home orders prior to March 28th, to those that issued orders after. We will compare states that started their reopening process prior to May 9th, to those that started later. And we will compare states that were surging as of June 23rd, to those that were remaining stable or improving at that time. Additionally, we will also look at states that have experienced exponential growth in infections over the past few weeks.

For states that implements stay-at-home orders prior to March 28th, between March 28th and May 9th, businesses in these states operated at 74% of normal levels. Since May 9th they have been operating at 96% of normal levels, which is down 2% from last week. Meanwhile, businesses in states that didn’t implement orders until after March 28th, only operated at 22% of normal levels prior to May 9th, and 67% of normal levels after May 9th, which is also down 2% from last week.

For states that started the reopening process prior to May 9th, businesses in these states were operating at only 25% of normal levels prior to May 9th. They are now operating at 50% of normal levels since May 9th, a 1% decrease since last week. However, businesses in states that waited until after May 9th to start their reopening process were operating at 61% of normal levels before May 9th, and have been operating at 100% since May 9th, a 2% decrease since last week.

For states that were surging as of June 23rd, businesses had been operating at 49% of normal levels prior to May 9th, and since have been operating at 64% of normal levels, marking no change since last week. In states that had COVID-19 under control as of June 23rd, businesses were only operating at 44% of normal levels prior to May 9th, since that time they have been operating at 113% of normal levels, a 5% decrease since last week. It is important to note that many of the states that had stable or declining infection rates as of June 23rd, now have rising infection rates.

New this week, we will be looking at one more number, we will look at the states that have experienced exponential growth in infections over the past few weeks. Those states are Arizona, Florida, Louisiana, South Carolina, and Texas. While Louisiana was one of the hardest hit states early on in the pandemic, they seemed to had gotten the virus under control up until about a month ago. The other four states had relatively low case counts early on, but now appear to be having infection rates that rival what New York saw at the start of the pandemic. Businesses in these states, all of which are heavily reliant on tourism, were operating at a dismal 18% of normal levels prior to May 9th, and since then have only been able to recover to 48% of normal levels.

Looking at the US as a whole, the nation’s economy was operating at 47% of normal levels prior to May 9th, and has been operating at 81% of normal levels since then. While we can not say that the economy of the US has recovered, it does at least appear to have stabilized for now. However, given the horrible numbers coming out of Arizona, Florida, Louisiana, South Carolina, and Texas, which typically make up about a quarter of our nation’s economy, it is easy to see how the economy could quickly stumble again if the nation fails to get COVID-19 under control.

- America

- Small Business

July 2, 2020

Categories:

Has the Economy Recovered from COVID-19?

As has been the case for the last few weeks, the data we have from this week appears to be remaining stable. This of course begs the question, has the economy recovered? While certainly plenty of damage has been done to the economy, there is no doubt that the economy has bounced back significantly and may have possibly reached its “new normal”. This week, given that the month of June has come to a close, we will be doing a month by month comparison, comparing 2020 to the years 2017-2019.

Purchase Orders

Credit approval requests were slightly down this week at 73% of normal levels, after reaching 78%, 76%, and 81% over the previous three weeks. Total dollars seemed to have stabilized as well at 78% of normal levels, after hitting 147%, 78%, and 101% during the previous three weeks, with that 147% primarily be driven from a single extremely large purchase order. While these numbers may not be very promising, these percentages are calculated against an annual average and does not take into account monthly fluctuation.

Comparing the approval volume from 2020 to the average volume between 2017 and 2019, we will find that January 2020’s volume was pretty much normal, at 93% of the volume we experienced in the Januarys of the previous 3 years. February 2020 began to show a slowdown as the volume was only at 77% of previous years’ Februarys. While COVID-19 may not have appeared to be a problem in the US back in February, it was already creating supply chain problems for importers from China and elsewhere in Asia, and this could help explain the decline in volume. The pandemic didn’t really impact the US until March, and it was only the final week in March when the first stay-at-home orders were put in place and businesses were forced to close, as a result volume was down to 61% of previous years’ Marchs. April of course was the height of the pandemic and volume in April plummeted to 43% of previous years’ Aprils, and only improved slightly in May to 48%. However, as many stay-at-home orders began to get lifted towards the end of May and most businesses were able to open up in June, June’s volume climbed to 96% of previous years’ Junes. It will be interesting to see if July can stay on pace, but this monthly data is a very strong indication of an improved economy as it averages out all of the weekly fluctuations we have been seeing.

Purchases

If we ignore the one very large purchase we had last week, purchases remained steady this week at 69%. While this may not be as high as they had been at the start of the month, it is still a very significant improvement over earlier in the pandemic when they averaged only 52% during the months of April and May.

We’ve been saying all along how purchases tend to fluctuate wildly from week to week, which of course makes the data a little hard to read. However, if we aggregate the data by month, as opposed to by week, those fluctuations should be flattened out. It is also important to note that the weekly data was being compared to annual average, and it too does not account for normal monthly fluctuations. So starting with January, we found that this year’s purchases were 92% of the average January from 2017 to 2019, which is perfectly in line with what we saw from approvals. Furthermore, supply chain problems in Asia would not have been impacted at this point in time as any ships would have departed prior to the first reported cases of COVID-19 in China. February saw purchases drop to 74% of the previous three years’ Februarys, quite possibly due to supply chain issues that emerged in Asia back in January. Purchases in March dropped further to 67% of the previous three years’ Marchs, as businesses began to shutdown at the end of the month and stay-at-home orders began to get implemented. April of course continued the descent to 44% of previous Aprils’ purchases, as some businesses were still open at the start of the month, and others still accepted orders placed prior to stay-at-home orders. Purchases bottomed out in May at 37% of the average May over the previous three years. However we did see a major rebound in June when purchases climbed to 59% of June’s average over the previous three years. The large discrepancy between purchases and purchase orders is due to the fact that purchase data tends to lag behind purchase order data be several weeks as it takes time to put together the orders, especially the larger orders that make up the bulk of these numbers. June’s purchase order numbers should be a very strong indication that purchases will return to near normal levels in July.

Payables

Payables continue to remain on track and heading in the right direction all across the board. Total outstanding dollars are up 5.5% making this the 5th consecutive week of growth, while the number of accounts with an open balance and the number of open receivables both climbed by 9%. Meanwhile, extremely past due invoices continued to get paid down this week.

While we did see an increase in current receivables, with total number up 1.7% and total dollars up 2.8%, these numbers aren’t growing as quickly as they had over the past few weeks. Still 72% of all receivables and 83% of all dollars are current, which is well above what would be considered normal. Even more amazing is that current dollars are now at 97.5% of where they were at on March 1st.

Meanwhile, the 1-30 day past due bucket made it first very significant increase since mid-April. The number of invoices in this bucket grew by 25%, while total dollars in this bucket grew an amazing 60%. Despite these large increases, there is little cause for alarm as it is probably due to the increase in current receivables that began at the start of June. Furthermore, the number of invoices still only account for 20% and total dollars only account for 10% of all receivables, again, both well below what would be considered normal. When you add up both the numbers and dollars that are either current or in the 1-30 days late bucket, they are within 2-3% of what would be considered normal. This is most likely due to the declining, but still unusually large amount of severely past due invoices, combined with slower purchases over the past two months due to the pandemic.

The 31-60 days beyond terms bucket also continued its sharp decline this week, with total numbers dropping by 25% and dollars dropping 39%. These invoices now only account for 1.8% of all invoices and 0.5% of all dollars. Both of these numbers are less than half of what would be considered normal, which is not surprising given that all these invoice were created in the month of April when businesses would have been well aware of the challenges that they would be facing.

Last week we saw some very worrisome data where invoices that were more than 61 days beyond terms seemed to only age further, with very little getting paid. Luckily this week saw some significant progress, both with invoices that are 61-90 days late and invoices that are over 91 days late. We saw a 12% decrease in the number of invoices and a 8.5% decrease in total dollars across these two buckets. These invoices now only account for 6% of both number of invoices and total dollars outstanding. While this percentage is unusually high, we are definitely seeing progress in this category, and the start of this week has seen several more of these invoices getting paid off which should lead to more good news next week.

State-by-State

Once again, it appears that businesses in states that have taken greater precautions in preventing the spread of COVID-19, have not only outperformed those in states that were less precautious, but that business in these states has indeed returned to normal levels. Whether we compare states that closed either before or after March 28th, states that reopened either before or after May 9th, or states that were experiencing surging COVID-19 rates as of June 23rd to those that were remaining stable or declining, businesses in states that took a stronger stance against the virus and managed it better are outperforming their peers.

When we look at states that implements stay-at-home orders prior to March 28th, we can see that from March 28th through May 9th, businesses in these states operated at 74% of normal levels, and since May 9th have been operating at 98% of normal levels. Businesses in states that didn’t implement orders until after March 28th on the other hand, only operated at 22% of normal levels prior to May 9th, and 69% of normal levels after May 9th.

Looking at states that began reopening prior to May 9th, businesses in these states were operating at 25% of normal levels prior to May 9th, and have been operating at 51% since May 9th. However, businesses in states that waited until after May 9th to reopen have fared much better, operating at 61% before May 9th, and 102% since May 9th.

Unfortunately, at this time COVID-19 cases appear to be surging across the country, including in states that seemed to have gotten the virus under control over the past two months. However, with approximately half the states surging as of June 23rd, that still seems an appropriate date to use for making comparisons. Businesses in states that were surging had been operating at 49% of normal levels prior to May 9th, and at 64% after May 9th. While businesses in states that weren’t surging as of June 23rd actually fared worse prior to May 9th, only operating at 44% of normal levels, but have done much better since May 9th, operating at 118% of normal levels.

What is most interesting is the progression we see from states that were first to close, to states that waited longer to reopen, to states that appeared to have the virus under control. The businesses in these states seemed to do progressively better in each comparison, which would indicate that taking the measures necessary to contain the virus is actually in the best interest of businesses, even if it means that they may not be operate for an extended period of time or forced to operate at reduced capacities. The fact that states that weren’t surging as of June 23rd have gone from worse to much better than their peers, shows that regardless of how the state tackled the virus early on, what matters most is what they are doing now to contain it. In other words, every state who acts appropriately now to contain the virus should be able to strengthen their economy, regardless of how they handled the pandemic in the past. Clearly consumers feel more confident spending their money when there is less risk of getting sick in the process.

While the economy hasn’t returned to normal yet, it does appear that it may have returned to normal in the states that have acted responsibly in controlling the COVID-19 pandemic. It also appears that the economy may have reached a level that could be considered a “new normal” at least until a vaccine becomes available. Of course, if states that are experiencing surges right now, such as Florida, Texas, and Arizona, can get the virus under control, it is quite possible that the economy could experience a full recovery. Only time will tell if this is indeed the case.

- America

- Small Business

June 24, 2020

Categories:

Economy Remains Strong as COVID-19 Cases Surge Around the Country

Once again we are continuing to see strong numbers from our data, although the numbers seem to be remaining stable now. This is still very good news as the economy has recovered immensely over the past few weeks and is approaching normal levels. However, with outbreaks spreading across the South and West, we are starting to see the economy slip in these regions. It will be interesting to see what the economy does over the next few weeks, especially if businesses may be forced to close their doors once again.

Purchase Orders

The number of credit approval requests we received this week hasn’t really changed much from the past two weeks, and are at a very acceptable 78% of normal levels, following 76% the week before and 81% the week before that. The big change was that total dollars jumped considerably to almost 150% of normal levels. While this may sound like fantastic news, it is entirely due to a single extremely large purchase order that we received. If we remove that one purchase order, total dollars for the week would be at 89% of normal levels, which also falls right in the middle of the numbers from the previous two weeks. This huge difference demonstrates just how much of an impact major retailers can have on the total dollars, but the relatively large number of approval requests does indeed that many small businesses are once again ordering.

Purchases

Purchases jumped this week to 122% of normal levels, however, this is mainly due to the fact that we purchased about three quarters of that very large purchase order we received this week. If we exclude this one very large purchase, purchases were only at 68% of normal levels. While that number is significantly lower than the 76% and 88% numbers we saw the previous two weeks, it is still much improved over what we saw at the height of the lockdowns. These numbers also seem to fluctuate wildly so a low number for one week isn’t really a cause for concern.

Payables

Once again payables look to be headed in the right direction and are growing significantly. Our total dollars outstanding the week are up nearly 16%. Now of course that includes the one very large PO, but even we exclude that, total outstanding is still up 3%, marking the 4th straight week of positive growth. Also growing are the total number of outstanding receivables which are up 7%, and the total number of accounts with a balance which is up 9%. Of course, all of this occurred as many older invoices continued to get paid off.

The number of invoices that are current grew by nearly 14% this week. Current invoices now account for 72.5% of all outstanding invoices, when normally they would only account for around 66% of all outstanding invoices. Current dollars grew by 25% this week, and if we were to eliminate that one large order they still would have grown by 8.5%. Current invoices now account for 85% of total outstanding dollars, way above the normal level of 77%. Most likely these unusually high percentage are due to the economy picking up after being quiet for so long. It will be interesting to see if these numbers are able to hold steady over the next 30 days.

The number of invoices in the 1-30 days late bucket actually grew slightly this week, however, they make up a slightly smaller percent of all outstanding invoices, still accounting for about 17.5% of all outstanding invoices. Meanwhile the total dollars in the 1-30 days late bucket dropped by 25% this week, and they now account for less than 7% of total outstanding dollars. Last week these invoices accounted for 10% of total outstanding dollars, and normally they would account for approximately 15% of total outstanding dollars. This huge decrease is due to invoices being paid for in a very timely manner, they are not aging out of this bucket.

This leads us to the 31-60 days beyond terms bucket. Once again, we saw a drastic decrease in this bucket. We saw 37% of these invoices which accounted for 59% of all dollars in this bucket get paid for in the last week. These invoices now account for only 2.7% of all outstanding invoices, which is down from a high of 23% from 6 weeks ago. 2.7% would actually be on the low side of what would be considered normal for this bucket. These invoices also account for less than 1% of total dollars outstanding, down from a high of 12% also from 6 weeks ago. Once again, this number would be on the low side of what is considered normal. All of these invoices would have been created after the initial stay-at-home orders went into effect, although it is possible that some of the orders would have predated the pandemic.

The more worrisome numbers are coming from invoices that are more than 61 days beyond terms. These numbers haven’t really changed any from last week, although a quarter of the invoices that were 61-90 days beyond terms last week, have now aged into the 91 days or more beyond terms bucket. These invoices still account for about 7.5% of all invoices and all dollars outstanding, while normally they would only be 3-4%. Of course, that 7.5% is a little inflated as we are only at approximately 78% of normal total volume. A large percentage of these invoices are coming from clothing stores, hotels, and restaurants, industries that were particularly hard hit by the stay-at-home orders.

State-by-State

Since we started doing state-by-state analysis of our data we have been sounding a lot like a scratched record, the states that opened prior to May 9th are fairing much worse than the states that waited later to reopen. Now as COVID-19 cases are surging across the country, we are actually seeing the economies of states that opened early start to slow down again, while those that waited longer continue to pick up steam. Furthermore, businesses in states that reopened early are still twice as likely to be past due than those in states that waited longer to reopen. However, our new discovery this week comes from comparing states that have managed to control the pandemic to those that are seeing a surge in cases.

As we mentioned, states that reopened earlier accounted for 40% of our volume prior to the pandemic, and slipped down to 21% of our volume at the height of sty-at-home orders. After reopening they started to gradually improve and last week we reported that their share of total volume increased by 3% since April 24th and 6% since May 9th. However, as many of these states have been hit by a surge in cases, those gains have all been pretty much wiped out. In just one week they lost all the gains they made since April 24th, and have now only gained 2% since May 9th. The reason behind this is that their total volume simply isn’t growing as quickly as total volume in states that waited longer to reopen. Since May 9th, states that reopened early are now at 49% of normal volumes, up from 25% prior to that. Meanwhile, states that reopened later are now at 104% of normal volumes since May 9th, up from 60% prior to that. Overall, the country is at 84% of normal levels, up from 47% prior to May 9th.

This week, given the huge surge in COVID-19 cases, we decided to compare states that are surging to those that are either improving or staying the same. It probably won’t come as a surprise that the states that are not seeing a surge in cases are doing much better economically. The states that are surging are currently doing 63% of their normal volume, up from 49% during the height of stay-at-home orders, while the states that are improving or staying steady are doing 122% of their normal volume, up from 44% during the height of stay-at-home orders. Of course, these numbers are both much higher than the numbers above, but that is due to the fact that many of the larger states, including California, Texas, and Florida, are states that are surging. Combining these numbers you still wind up at the same 84% for the country.

Since we can see such a large difference between states that are surging and states that aren’t, it probably would make sense to see if there was a similar trend at the start of the pandemic. To do this, we will compare states that issued stay at home orders prior to March 28th, to those that waited longer or never issued stay-at-home orders. Interestingly, both of these groups accounted for 50% of our volume prior to the pandemic. During stay-at-home orders, the states that were quicker to enact orders saw their volume reduced to 74% of normal levels during the stay-at-home orders, but that volume has since recovered to 96% of normal levels as stay-at-home orders began to get lifted. However, in states that waited to enact orders, their volume dropped down to 22% of normal levels immediately after California issued the first stay-at-home orders. As stay-at-home orders began to get lifted, these states saw their volume improve to 72% of normal levels.

What’s interesting is that states that reopened earlier clearly did so because their local economies were completely destroyed by the pandemic. However, when we compare the states that are surging to the ones that aren’t, we can see that their economies were pretty much the same during stay-at-home orders. Whether or not a state chose to reopen early or not does not correlate with whether there is a surge in the state. While Texas, Florida, and Georgia all reopened early and are experiencing surges, California waited to reopen but are still experiencing a surge. Furthermore, Indiana, Colorado, and Maine reopened early, yet the number of cases in those states is either staying steady or declining. We also saw that the states that acted sooner in issuing stay-at-home orders also fared much better during the lockdown, and have continued to do better since. From the data above we can see that consumers are definitely concerned about their health, and are more willing to spend money if they live in a state that is taking greater precautions to minimize the spread of disease. As states continue to open up more and more, if that reopening up leads to a surge in cases, then there is very little to be gained economically from the reopening. However, if the reopening is done responsibly, the economy can thrive even if many restrictions are still in place.

Certainly, there is a lot of information that can be learned from the data, and as the situation in both the country and each state changes, we are seeing some very interesting things happen. Here at DSA Factors we will continue monitoring and reporting on our data for as long as we need to. Let’s hope that we won’t need to do so for too much longer.

- America

- Financing

- Fintech

- Insurance

- Retail

- Small Business

June 19, 2020

Categories:

The Dangers of Supply Chain Finance in the COVID-19 Era

Supply Chain Finance has been gaining in popularity over the past few years. Instead of forcing vendors to wait 30 or 60 days to get paid for their receivables, retailers have discovered that they can get a several percent discount in exchange for paying their vendors early. It seemed like a win-win, vendors get the cash flow they need, and large retailers get a discount at a rate that far exceeds interest rates. Of course, all of this changed over the past few months as our nation, and the world, have been gripped by the COVID-19 pandemic.

Suddenly, retailers have been forced to shut their doors with no plan for when they may be able to reopen. While their customers have been laid off, furloughed, or taken pay cuts, and those who have managed to maintain their jobs are more concerned with purchasing essentials and saving money in case they too become an economic casualty of the COVID-19 pandemic. Not to mention, many consumers simply don’t feel safe leaving their homes for anything that isn’t essential. As a result, these retailers have found it best to hold onto their money for as long as they can, and most have either extended payment terms (with or without permission) or are simply paying invoices well beyond the due date. For small vendors that have relied on supply chain finance, they now find themselves in a very difficult position.

One of the major retailers who offers supply chain financing is TJX (TJ Maxx, Marshalls, Homegoods). When stay at home orders were first issued, TJX told all their vendors that they would be extending terms on all of their invoices from 30 to 90 days, although they reversed that decision a couple weeks later due to the backlash they received from the vendors. However, by that point the damage had already been done. Many vendors were unable to get the early payment they rely on, and due to the closure of their corporate headquarters and a need to catch up, many invoices were still paid well beyond terms. Companies that were used to getting paid within 5-10 days were now waiting 45 days to get paid, and this was at a time when sales had pretty much dried up. It also appears that for the immediate future, any new orders from TJX will have terms of 90 days, making it unlikely that they would be willing to offer early payment. Unfortunately, TJX was far from the only major retailer to extend terms or simply fall behind on their bills.

Of course, it also isn’t just an issue of cash flow anymore, the COVID-19 pandemic has proven to be just as deadly for businesses as it is for the people it infects. While all non-essential businesses had been forced to close their doors temporarily to flatten the curve, many of these businesses will be closing them permanently as a result of no revenue but continuing expenses. If the retail apocalypse wasn’t bad enough before the pandemic, the recent wave of bankruptcies has been incredible. Already we have seen J.C. Penney, Neiman Marcus, J. Crew, Stage Stores, and True Religion have all filed bankruptcy during the pandemic. Lord and Taylor has avoided bankruptcy, but has announced they will be holding going out of business sales as soon as they are allowed to reopen. L Brands (Victoria’s Secret, Bath and Body Works) will not be filing, but will be permanently closing 250 stores. While Pier 1 Imports and Art Van Furniture, both who filed bankruptcy prior to stay-at-home orders being issued, were forced to change their bankruptcy plans and completely liquidate. Of course, the retail sector is far from the only industry being hit with bankruptcies, hospitality, entertainment, and health clubs have also been filing for bankruptcy at an incredible rate. Sadly, these companies are only the beginning, with many more considering their options as well.

Even worse, the dangers of bankruptcy are actually compounded by supply chain finance. Many businesses don’t feel the need to carry credit insurance if their customers offer supply chain financing. The logic behind this is that there is no risk if a company is paying them early. However, the decision to pay early is entirely up to the customer, as is the amount of the discount that they will take. Prior to filing for bankruptcy in 2017, Toys’R’Us utilized the popular C2FO platform for supply chain financing. Towards the end they started demanding larger and larger discounts in return for early payments. Further complicating matters is US bankruptcy law in regards to receiving preferential payment. When a company files for bankruptcy, the bankruptcy court can demand that any preferential payments made within 90 days of the filing be returned to the court. When a vendor offers a discount in exchange for an early payment, there is no question that the vendor has received a preferential payment and will be forced to return the payment to the court. So vendors that offered double digit discounts that Toys’R’Us accepted, ultimately would have had to return the funds if they were received within 90 days of the filing. Had they waited until the invoice was due and gotten paid in full, they probably would have been able to keep their money.

With many businesses reopening at this time, there is still a question of how many of them will be able to survive. With consumers spending less money these days, and spending in unpredictable ways, combined with a fear of whether it is even safe to go out in public, revenues will continue to remain low for the foreseeable future. Yet these companies will need to rehire much of their workforce and continue to make rent, pay utilities, and interest payments on debt. For businesses such as restaurants and movie theaters, who will need to reopen at reduced capacities, there is a question as to whether or not they will be able to remain profitable. Unfortunately, most experts are predicting that even though businesses are starting to reopen now, many businesses that have survived so far might not make it through to the end of the year. Even with companies that emerge from the lockdowns with strong sales, there is still the question of whether or not they would be willing to pay invoices quicker, the current trend is that most companies are requesting longer payment terms. Of course, none of this takes into account the possibility of a second wave of infections and subsequent closures.

Relying on supply chain financing to improve your cash flow may have worked for the last few years, but it is doubtful that it will be as reliable moving forward. Furthermore, wholesalers need to be more careful than ever about who they are selling to. The only thing worse than getting paid slowly is not getting paid at all. Paying for credit insurance on top of supply chain financing can be extremely costly, especially for businesses that do less than $10 million a year. Not to mention, the credit insurance companies have been hesitant to take on new clients, and have slashed credit limits across the board for their existing clients.

There is a solution to this problem, and that is accounts receivable factoring. With accounts receivable factoring you sell your receivables to a factoring company, and can be funded the same day you ship the merchandise, making it a much quicker turnaround than supply chain finance. Furthermore, your factoring company is responsible for monitoring your customers and establishing appropriate credit limits. If the factoring company offers non-recourse factoring, then not only do you receive improved cash flow, but they also insure your receivables, eliminating the need for costly credit insurance. Just like supply chain finance, when you factor your receivables you are not taking on any new debt as your factoring company is purchasing your receivables from you. The best part, however, is that accounts receivable factoring is available for all of your accounts and costs no more than supply chain financing. Plus, since factoring rates are fixed, it takes away all the guess work associated with supply chain finance and can easily get built into your margins. Want to learn how easy it is to improve your cash flow with accounts receivable factoring? Give DSA Factors a call today at 773-248-9000 and we will be happy to speak with you.

- America

- Small Business

June 17, 2020

Categories:

Another Strong Week as the Economy Returns to Normal During the COVID-19 Pandemic

Last week we had reported our strongest week yet since stay-at-home orders were implemented to slow the transmittal of COVID-19. While this week’s data isn’t quite as strong as last week's, it is still stronger than any other week’s data that we have seen throughout the pandemic, and a very strong sign that the economy is recovering to near normal levels.

Purchase Orders

This week we saw a very minor decline in the number of approval requests we received. With the number of requests falling to 76% of normal levels from last weeks 81%. Meanwhile total dollars had dropped from 101% of normal levels last week to 78% of normal levels this week. The drastic decline in total dollars compared with the minor decline in number of requests would imply that our clients received fewer purchase orders from major retailers than they had the previous week, although purchase orders from small businesses would have remained steady. Of course, last week’s data was coming on the heels of poor data the previous week, so it is quite possible that last week’s data could be the result of slow reporting of the previous weeks data. Regardless, the data we collected this week is very promising, and while it is too low to be considered within a normal range of fluctuation, it is a very promising sign that the economy is headed in the right direction.

Purchases

Purchases have been harder to gauge as they seem to fluctuate wildly from week to week. However last week we reported purchases reached 76% of normal levels which was our second strongest week yet, and the only stronger week being early on in the pandemic when we had several very large purchases from major retailers, all from purchase orders placed prior to the pandemic. This week purchase levels reached 88% of normal levels, which is nearly a 250% increase over the lows we experienced just one month ago. In fact, purchases have now increased in 4 of the last 5 weeks since we experienced that low.

Payables

Payables are continuing on their path to recovery. It appears that the businesses who are placing orders are in a position to get them paid off promptly, and the vast majority of businesses who placed orders just prior to the start of the pandemic have now paid for those orders. However, it does appear that businesses that were struggling prior to the pandemic are still struggling as very few of them are making progress in paying off their old invoices.

Total outstanding dollars are up again for the third straight week, this time increasing by 3% after increase of 2% and 1% in the previous two weeks. This increase has also coincided with over a third of very past due invoices being paid off over the same period. When looking at current dollars, they climbed nearly 6% this week after they climbed by 13% last week, which was the first time we started to see them rise. 79% of all dollars are now current, which is the highest level we have seen yet, and slightly better than what would be considered normal.

In terms of number of outstanding invoices, we have seen much more dramatic increases. They rose by 12% this week after climbing by 4.5% the week before. The number of accounts with outstanding invoices grew in a similar way, climbing 15% this week after a 7% climb last week. The inverse relationship between the growth in number of invoices and accounts compared to total dollars would suggest that much of the business that occurred over this past week had been with small businesses. At this point, nearly 70% of outstanding invoices are current, which is significantly above the 66% that would be considered normal.

This week only 17.5% of all receivables are now 1-30 days beyond terms, and they account for 10% of total outstanding dollars. Neither of these numbers have really changed much from last week, but they are still well below normal levels. This would seem to imply that only businesses that can afford to pay for their merchandise in a timely fashion have been placing orders during the pandemic. However, what we don’t know is if this is due to these businesses seeing an uptick in sales, or if they are simply strong financially and confident in their ability to recover.

Another very promising sign is what is happening with receivables that are 31-60 days beyond terms. 39% of these receivables and 47% of the total dollars in this category have gotten paid off over the last week. At this point, almost all of these invoices would have been created during the pandemic, although it is possible that some of the orders were placed just prior to the start of the pandemic. We saw the number in this aging bucket peak just 5 weeks ago when they accounted for 23% of all outstanding invoices and 12% of all outstanding dollars. Today they only account for 4.6% of all invoices and 2.5% of all dollars. We have experienced an 81% decrease in both the number of receivables and total dollars in this category over this 5 week period. Of course, the invoices in this category 5 weeks ago would now all be in the 61-90 days past due category, and the invoices in this category today would have been in the 1-30 days past due category 5 weeks ago. However, 5 weeks ago invoices that were 1-30 days beyond terms made up 33% of all invoices and 17.5% of all dollars. That is a pretty drastic improvement, and while these numbers may still be a little high, they are only maybe 1% off from normal levels.

That of course brings us to invoices that are more than 61 days beyond terms. The good news and the bad news is that the number of invoices and total dollars in this category has not changed significantly over any of the previous 5 weeks. While the bad news would be that newer invoices have aged into this category over the past 5 weeks, the good news is that an equal number of invoices have been paid from this category over the same 5 weeks. In other words, invoices that were problematic 5 weeks ago are less problematic today, but there are an equal number of new invoices that have since become problematic. It is important to keep in mind that the invoices that are 61-90 days past due would have all been created prior to the first stay-at-home orders, but would have become due after the orders were issued. The vast majority of the accounts in this category are for clothing retailers, including major department stores, and businesses in hospitality such as restaurants and hotels. Nearly all of the invoices that are more than 90 days beyond terms, were already severely past due when businesses were forced to shut down, many of which were on payment plans that they have failed to keep up with as a result of the pandemic.

State-by-State

Once again, for the states that reopened early, prior to May 9th, their economy seems to be trailing behind the economies of states who waited longer to reopen. While they are doing slightly better after this last week, we have only seen their percentage of total volume climb by 3% since April 24th, when Georgia reopened, and by 6% since May 9th, after having dropped by 20% during the height of stay-at-home orders. While all states are recovering, the recovery is happening quicker in states that waited longer to reopen. The states that reopened early are now operating at 44% of normal levels, up from 25% during stay-at-home orders, while states that waited longer to reopen are now at 88% of normal levels, up from 60% during stay-at-home orders.

It has also become clear that businesses in states the reopened early are having a more difficult time paying down their balances. While businesses in these states had the upper hand initially after their states reopened, now that pretty much every state has reopened to some extent, businesses in states that reopened later are doing a better job of catching up on past due invoices. Only 2% of invoices that pre-date stay-at-home orders are still open in states that waited longer to reopen, but 5% of these invoices are still outstanding in states that reopened early. While the states that reopened early accounted for 40% of our volume prior to the pandemic, they now account for 60% of all open invoices that date back to before the pandemic.

The decision on when to reopen appears to have been made heavily on the state of the local economy in each state, but it certainly does not appear to be the case that reopening earlier has had much of a positive effect on the states that chose to do so. Rather it seems that how strong a local economy was during stay-at-home orders has a direct correlation to how quickly that economy has been able to recover. In the meantime, it is becoming very clear that reopening has led to a surge in COVID-19 cases, even in states that waited longer to reopen. While it was major cities and their suburbs that were hit the hardest early on, some of the highest rates of infection are now occurring in small towns and rural areas. If states are forced to close again, it could be devastating for the businesses that are just starting to bounce back from the first lockdown. DSA Factors will continue to monitor and report on the situation as it continues to evolve.

- America

- Small Business

June 10, 2020

Categories:

Major Economic Improvements This Week as Businesses Start to Return to Normal

We reported last week that we saw a slight slowdown in the recovery of our nation’s economy. But our data from this week suggests that is most likely an outlier, or possibly just a slight delay in receiving this week’s data to analyze. For the first time since stay-at-home orders were issued at the end of March, we are now seeing data that appears to be at near normal levels. This of course reflects the larger picture that has emerged in the national news with unemployment levels falling in May and the stock market bouncing back to pre-pandemic levels. But it also comes during a week of large, organized protests all across the country, and looting that has occurred in many cities and suburban areas.

Purchase Orders

Last week we saw the number of credit approval requests and the total dollars requested return to pre-pandemic levels. The number of credit approvals requested was at 81% of average, which is well within a normal level of fluctuation that we see week to week. In terms of dollars, they were at 101% of average. While it is certainly possible that this week’s data could be an outlier, or it could be that some purchase orders that came in the previous week didn’t get submitted to us in a timely fashion, there is no question that this is indeed good news. The highest numbers that we had seen for requests and dollars were only 52% and 78% respectively. We haven’t seen numbers like this since the week ending March 20th. Now it is a little concerning that the percentage for number of requests is much lower than the percentage for dollars requested, as this would imply the major retailers are accounting for the majority of the volume. But just how drastically both these numbers have improved over the last week would imply that many small businesses are recovering as well.

Purchases